Europe’s reverse-charge regime is moving tax risk from invoices to the retail edge. Fiscalization may become the next control layer.

VAT rarely looks like a retail strategy topic. It sits in finance departments, tax manuals and ERP configuration tables. Yet the European Parliament’s 2026 study on the VAT reverse charge mechanism tells a different story. Europe’s anti-fraud architecture is becoming a transaction-data architecture. That architecture will increasingly touch the systems retailers use every day: POS, e-commerce, invoicing, ERP, tax engines, fiscal middleware and reporting platforms.

The policy debate is technical. The business consequence is not. If VAT fraud control moves closer to the transaction, retail technology becomes part of tax enforcement infrastructure.

What the reverse charge mechanism actually does

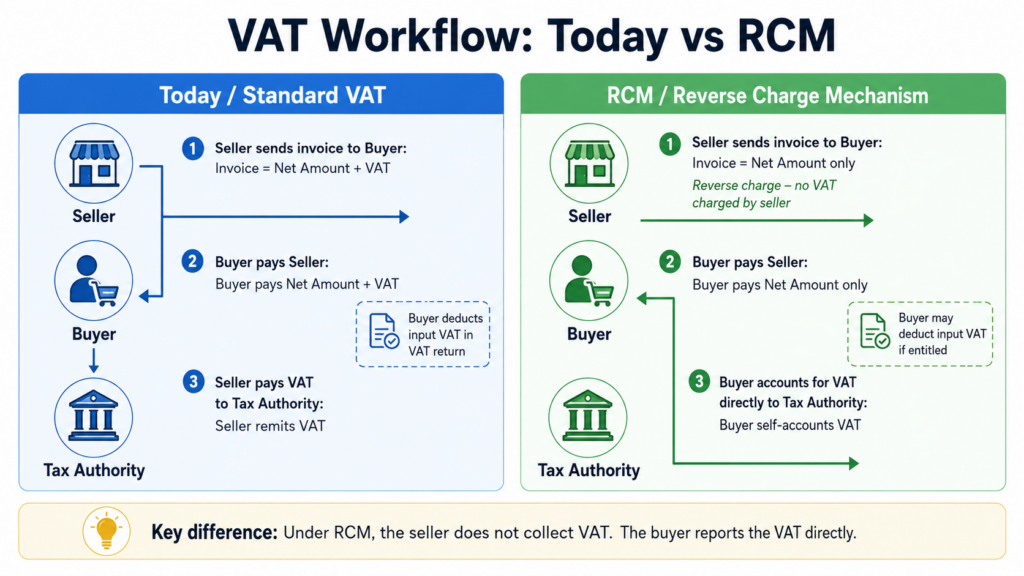

Under the normal VAT model, the supplier charges VAT to the customer, collects it and later remits it to the tax authority. The EU VAT system is built around collection at each stage of the supply chain, from production to final sale. That design collects tax gradually, but it also creates a fraud opportunity when a supplier collects VAT and disappears before remitting it. The European Parliament study identifies missing trader intra-Community fraud and carousel schemes as the core vulnerabilities behind the reverse-charge debate.

The reverse charge mechanism, or RCM, changes who accounts for VAT. In a transaction covered by RCM, the supplier does not charge VAT. The purchaser self-accounts for VAT in its own VAT return. The study describes this as a shift from supplier non-remittance risk to purchaser self-accounting, correct transaction classification, and deduction or refund integrity.

In plain language, RCM removes the VAT cash from the seller’s hands. That is why it is useful against missing-trader fraud. The fraudster can no longer collect VAT from the buyer and disappear with the money, at least for the transaction category covered by reverse charge.

What the quick reaction mechanism is supposed to do

The quick reaction mechanism, or QRM, is the emergency version of the same idea. Article 199a of the VAT Directive allows Member States to use reverse charge in predefined high-risk sectors. Article 199b is designed for sudden and massive fraud outside the predefined list. The study explains that QRM is meant to let a Member State apply reverse charge faster than the standard Article 395 derogation procedure, which can take up to eight months, while the Commission has one month to decide on a QRM application.

The logic is convincing. Fraud networks move quickly. Governments need a tool that can move before losses become permanent. The problem is that the tool has not worked in practice. The Parliament study states that QRM has never been activated since its enactment and that the only request submitted to the Commission was rejected. The study calls Article 199b legally available but operationally difficult to activate.

The status in the EU

Both mechanisms are already part of EU VAT law. The European Parliament study states that the RCM under Article 199a and the QRM under Article 199b remain in force until 31 December 2026. The same study was prepared because the European Parliament’s Subcommittee on Tax Matters is assessing whether these instruments should be prolonged, revised, recalibrated or allowed to lapse after that deadline.

The status is therefore clear. RCM is legally available and widely used, but not uniformly. QRM is legally available and not practically used. This difference matters for business planning. One instrument is embedded in national VAT systems. The other is a contingency tool that may be redesigned if policymakers want it to become operational.

Which countries use RCM

The country picture is uneven. The study finds that most Member States currently apply at least one Article 199a reverse-charge measure, but the scope differs substantially by country. Some countries rely on one narrow category. Others use reverse charge across a wider range of sectors. The study says implementation depends on national fraud-risk perception, sector vulnerability, economic structure, alternative anti-fraud tools and administrative choices.

According to Annex 3, Table 14 of the study, Article 199a measures were in force in 2026 in Austria, Belgium, Bulgaria, Cyprus, Czechia, Germany, Denmark, Estonia, Greece, Spain, Finland, France, Croatia, Hungary, Ireland, Italy, Lithuania, Luxembourg, Latvia, the Netherlands, Poland, Portugal, Romania, Sweden, Slovenia and Slovakia. Malta confirmed that it does not apply Article 199a of the VAT Directive.

The sectors are not random. The study reports that emissions allowances are the most common current category, applied in 22 Member States. Cereals and industrial crops are used by six Member States, telecom services by four, and the other Article 199a categories are used by between nine and 15 Member States. Poland is a special case because it replaced Article 199a RCM with mandatory split payment for four product categories in 2019, while later adding RCM measures for emissions allowances and gas and electricity.

What the report really finds

The report’s first message is that reverse charge works best as a targeted instrument, not as a general tax philosophy. The study gives a cautiously positive assessment of Article 199a. It appears most effective where the transaction environment resembles typical missing-trader or carousel fraud: high-value, fast-moving goods or services traded through B2B chains.

The second message is that reverse charge does not make compliance simpler. It changes the location of complexity. Tax authorities move attention from supplier non-remittance to purchaser accounting, refunds, transaction scope, monitoring and data matching. Businesses face higher costs where thresholds, mixed supplies, resale criteria, narrow supply definitions and divergent national schemes are present.

The third message is that monitoring is weak. The study says only limited monitoring and evaluation approaches exist at Member State level. Belgium was the only Member State reporting regular annual or biannual evaluation of RCM effectiveness as part of a larger risk-analysis exercise. Austria, Czechia, Finland, Lithuania, Poland and Sweden reported ad hoc evaluations, while some countries reported no regular evaluation at all.

The fourth message is that digital VAT control will reshape the debate. The ViDA package was adopted on 11 March 2025 and will roll out until 2035. It includes digital reporting requirements and e-invoicing, especially for intra-EU transactions; updated VAT rules for the platform economy; and expansion of single VAT registration. Digital reporting for cross-border B2B transactions is expected from 1 July 2030, while Member States with their own real-time reporting must align with EU standards by 1 January 2035.

The fifth message is decisive for retail technology. ViDA will not immediately replace RCM because the tools do different jobs. RCM removes supplier-side VAT cash-flow risk. Digital reporting and e-invoicing increase visibility. The study states that ViDA should strengthen the data environment by making it easier to detect misclassification, missing self-accounting, refund risks and fraud displacement to adjacent transactions.

Why this matters for retail

Retail enters the story through displacement. Reverse charge can close one fraud door in B2B distribution, but it can push pressure toward the final consumer transaction. The study calls this the last-mile problem. By removing VAT collection from B2B transaction steps, reverse charge can make the consumer transaction the last effective point of VAT collection. That point is harder to enforce.

Spain is the warning signal. The study reports that Spain saw patterns of fraudulent activity in mobile phone trade migrate from the wholesale step targeted by reverse charge toward retail counterparts, especially online sellers. The broader conclusion is even sharper: reverse charge does not prevent fraud entirely; it redirects fraud pressure toward harder-to-monitor segments such as retail, cross-border e-commerce and refund claim verification.

This matters for every retailer selling high-value, mobile or easily resold goods. Electronics, devices, energy-related goods and metals may sound like specialist sectors, but retail has become omnichannel, marketplace-based and cross-border. A fraud pattern that begins in wholesale can end in web shops, marketplace storefronts, consumer invoices and refund claims.

Retailers should therefore stop treating reverse charge as a remote B2B finance rule. The operational questions are retail questions. Is the customer a taxable person. Is the buyer a reseller. Is the product in scope. Does the threshold apply. Does the invoice need specific wording. Is the online order routed through the right legal entity. Does the ERP tax code match the POS or e-commerce treatment. Can the transaction be explained later to an auditor.

The connection with fiscalization

The report does not present itself as a fiscalization report. It is nevertheless highly relevant for fiscalization. Fiscalization is about trusted transaction evidence. The report’s recommendations point toward the same direction: more structured, verifiable, transaction-level data.

The study recommends strengthening transaction visibility through automated matching, invoice data, risk-assessment tools and integrated reporting systems. It argues that investments in data quality and analysis are likely to pay off better than overly complicated legal perimeters.

That is the fiscalization bridge. Traditional fiscalization focuses on B2C transaction integrity: receipt creation, signature, sequence, journal, transmission and audit evidence. RCM and ViDA focus on VAT chain integrity: invoice data, counterparty status, self-accounting, refund verification and transaction matching. These are different control layers, but they are converging around the same core asset: reliable transaction data.

For POS vendors and fiscalization providers, the future opportunity is not just compliance with local receipt rules. It is the creation of a compliance data layer that connects POS, e-commerce, ERP, e-invoicing, VAT reporting and audit trails. In this environment, fiscalization stops being a national cash-register obligation and becomes part of the wider European tax-control stack.

The business interviews in the study confirm the systems impact. Businesses reported that RCM implementation starts with system adjustments. The most common costs were ERP configuration, invoice-template updates and internal training. Once RCM applies, accounting, ERP and invoicing systems must be aligned and tested. The study says implementation typically requires changes to invoicing workflows, VAT coding, ERP configuration and VAT return mapping.

This is exactly where fiscalization and tax engines meet. Tax law becomes executable behavior. The company must know the rule, classify the transaction, configure the systems, test the output and preserve evidence. That is not a legal memo. It is a production system.

Future developments

The most likely future is not the end of reverse charge. It is extension with recalibration. The study explicitly says the preferred policy direction is neither expiry nor unconditional rollover. Article 199a should remain available beyond 2026, but its future use should be tied more clearly to fraud risk, proportionality, implementation quality and periodic assessment.

Businesses interviewed for the study also favoured continuation with clearer and more consistent rules. None of the interviewed businesses favoured allowing reverse charge to expire at the end of 2026. Their preferred improvements included clearer harmonised rules, a digital tool or register to verify customer or reseller status, simpler threshold treatment, sufficient lead time for changes and, in some cases, broader B2B application to reduce boundary problems.

The future of QRM is more uncertain. The study says Article 199b should be extended only if it becomes operationally more usable. Suggested reforms include clearer criteria, standardised risk-assessment and notification forms, a better relationship with Article 395 and more realistic duration or renewal periods.

The future of retail compliance will be shaped by three forces. The first is targeted reverse charge in high-risk B2B sectors. The second is ViDA-driven e-invoicing and digital reporting. The third is stronger control of the retail edge, especially online channels, where fraud can reappear after wholesale controls improve. Together they will push retailers toward more integrated tax architectures.

There will also be a stronger demand for counterparty verification. The study recommends clear definitions, standardised documents and potentially an EU-wide tool for verifying whether a customer meets reverse-charge requirements. For retailers with B2B and B2C channels, that could make customer tax status part of transaction logic rather than a back-office afterthought.

Thresholds will remain a problem. The report warns that thresholds can create fragmentation, invoice-splitting risks, higher IT costs and additional classifications. It recommends careful review and clearer guidance if thresholds remain. For retailers, this means that tax configuration will need stronger testing, monitoring and exception handling.

Conclusion

The reverse charge mechanism is often presented as a technical VAT tool. That is too narrow. It is part of a broader movement in Europe from periodic tax reporting to transaction-level tax control. RCM changes who accounts for VAT. ViDA changes how transaction data becomes visible. Fiscalization secures the retail transaction. Together, they point toward one conclusion.

The future of VAT enforcement will not only be written in tax law. It will be executed in retail systems.

For retailers, this means tax compliance is becoming an architecture decision. For POS and fiscalization providers, it means the market is moving beyond isolated national receipt rules toward integrated transaction-compliance intelligence. For tax authorities, it means anti-fraud policy will increasingly depend on data quality, system design and real-time visibility.

Europe may extend RCM after 2026. It may redesign QRM. ViDA will continue to roll out until 2035. The direction is already visible. VAT control is moving closer to the transaction. Retail is where many of those transactions end.

Source log and fact-check notes

European Parliamentary Research Service, “The implementation and impact of the VAT reverse charge mechanism in the EU”, PE 774.719, June 2026. Used as the primary source for definitions of RCM and QRM, current legal status until 31 December 2026, country usage, report findings, retail displacement, systems burden, recommendations and future policy direction. Page and line references are included throughout the article. Source: https://www.europarl.europa.eu/RegData/etudes/STUD/2026/774719/EPRS_STU(2026)774719_EN.pdf

European Commission, Taxation and Customs Union, “VAT in the Digital Age (ViDA)”. Used to verify the adoption date of ViDA, the progressive rollout until January 2035 and the official policy framing of ViDA as a modernisation package for the EU VAT system. The article also uses the EPRS report’s page-and-line references for the detailed ViDA timeline. Source: https://taxation-customs.ec.europa.eu/taxation/vat/vat-digital-age-vida_en

Council Directive (EU) 2022/890 of 3 June 2022 amending Directive 2006/112/EC as regards the period of application of the optional reverse charge mechanism and of the Quick Reaction Mechanism against VAT fraud. Used to cross-check that Articles 199a and 199b were extended to 31 December 2026. The article cites the EPRS study for page-and-line support and retains this legal act in the source log for legal verification. Source: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32022L0890