Why retailers should keep e-invoicing close to ERP and accounting, while keeping fiscalization close to the point of sale.

The Architecture Mistake

Every new e-invoicing mandate creates the same temptation. A retailer already has a fiscalization layer, a fiscal middleware or a communication channel to a tax authority, so someone asks whether e-invoicing should simply be added there as well. The idea sounds efficient, at least in a meeting room. One more legal communication channel through the same compliance interface, one more country-specific obligation handled by the same team and same infrastructure. The reality is usually the opposite.

E-invoicing is not a document that can be solved by taking a B2B sales transaction from the point of sale, converting it into a required XML or structured format, and sending it to a government platform or a certified exchange provider. That is only the first and most visible transaction. The real e-invoicing world is a regulated invoice-lifecycle engine, with corrections, credit notes, debit notes, self-billing, cancellations, rejections, refund documents, advance payments, delivery references, lifecycle statuses, archiving and reporting for transactions that are not normal domestic B2B sales.

That changes the architecture discussion completely. If the majority of legally relevant e-invoicing processes already live in ERP, accounting and accounts payable systems, the attempt to place e-invoicing on the fiscalization layer creates duplication rather than simplification. It forces retailers to integrate the same business reality twice, split ownership between systems that were designed for different moments of the commercial process, and introduce a new source of failure into one of the most sensitive parts of the finance and tax architecture.

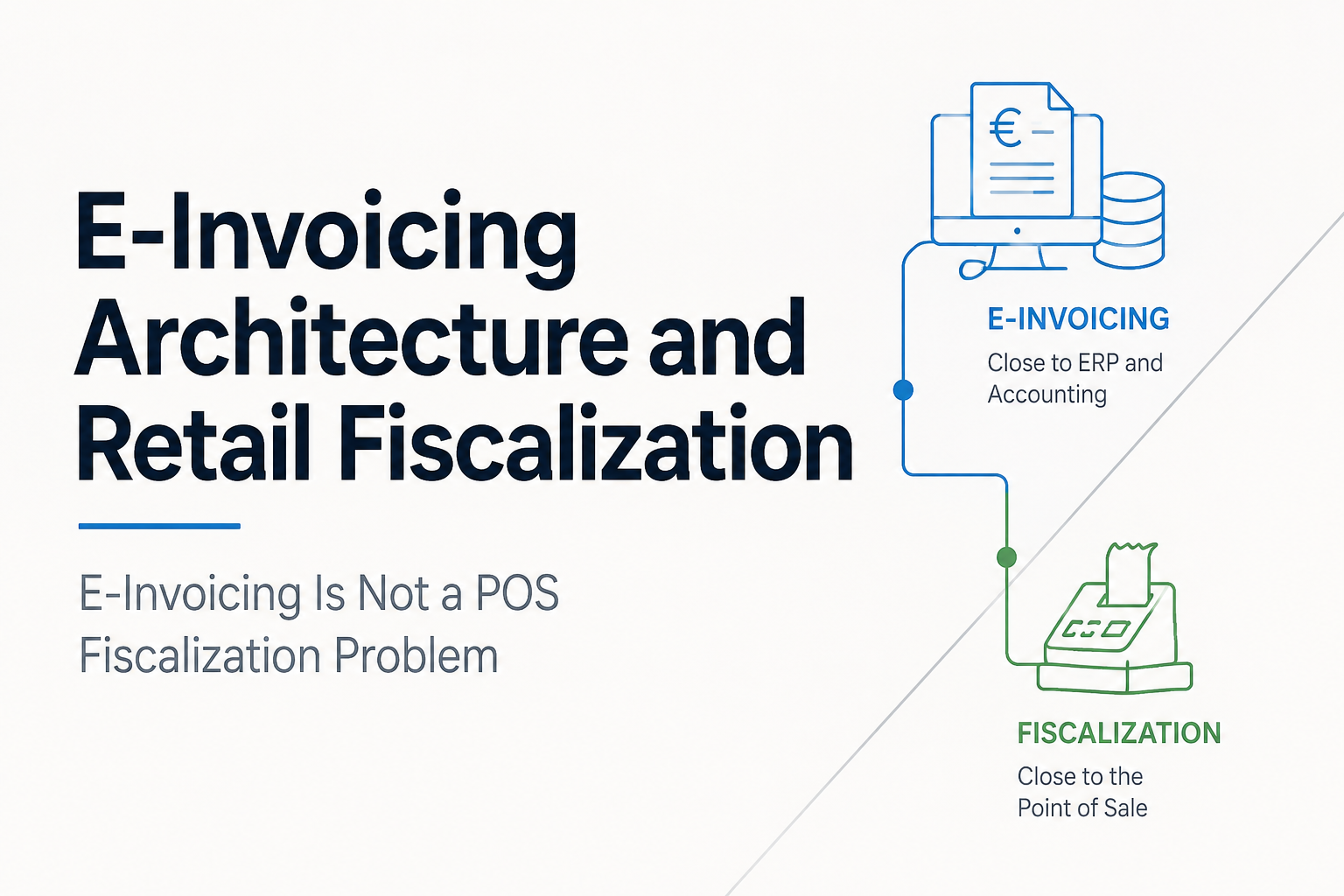

Fiscalization and E-Invoicing Start in Different Places

Fiscalization and e-invoicing are often mentioned together because both are driven by tax authorities and both use technical reporting obligations. For retailers, however, they solve different problems at different moments in the business process.

Fiscalization is close to the moment of sale, especially in B2C retail. It must work when a customer pays, when a receipt is created, when a return happens at the store, when a fiscal signature or code is needed, when the cash register must continue offline, and when the tax authority expects transaction evidence that reflects what happened at the point of sale. It is operational, real-time and store-facing. If it fails, the customer may be standing in front of the cashier.

E-invoicing is different. It belongs to the invoice lifecycle, and that lifecycle is already part of ERP, finance, tax and accounting. A B2B sales invoice may originate from a retail transaction, but the legal process does not end at the sale. It continues into accounts receivable, accounts payable, credit management, returns settlement, master-data validation, tax reporting, audit archive and often platform status management. These are not natural POS processes, and most global retailers have already invested heavily in ERP and accounting systems precisely because these systems own this complexity.

This is why the discussion should not start with the question of whether one vendor can technically connect to another government platform. It should start with process ownership. The owner of fiscalization is the retail transaction environment. The owner of e-invoicing is the financial document lifecycle. When those two ownership models are mixed incorrectly, the result is rarely innovation. It is usually architecture debt.

The Invoice Is Only the Beginning

The clearest evidence comes from the e-invoicing mandates themselves. The European EN 16931 logic and Peppol environments do not treat the invoice as a single commercial event. They support different invoice type codes and related document processes, including credit notes, self-billed credit notes, interim payment requests, final payment requests and other document types. Germany, through XRechnung and EN 16931-based rules, uses invoice type code logic to distinguish the legal character of the document, including credit-note and self-billing scenarios.

Italy shows the same pattern in a clearance model. FatturaPA documents are exchanged through the Sistema di Interscambio, and Italian document types include normal invoices as well as credit notes, debit notes and self-invoicing scenarios. Malaysia makes the lifecycle even more explicit in its MyInvois framework, where the official e-invoice type list includes invoice, credit note, debit note, refund note, self-billed invoice, self-billed credit note, self-billed debit note and self-billed refund note. France is moving toward a model in which B2B e-invoicing is combined with e-reporting for B2C and cross-border transactions, platform routing and invoice lifecycle statuses.

These are not marginal details. They are the law moving from invoice exchange to invoice governance. A retailer that builds only the outbound B2B sales invoice has not built e-invoicing. It has built the easiest visible fragment of e-invoicing.

Why the POS Is the Wrong Place for Most of This

A POS system can create a sales event, but it is not usually the system that owns all later financial consequences of that event. It does not normally own supplier self-billing, invoice reception, invoice rejection handling, accounts payable workflows, payment status updates, delivery-note references, long-term invoice archiving and financial settlement. It may trigger information that later becomes relevant, but it is not the natural system of record for the entire invoice lifecycle.

The same is true for fiscal middleware. A good fiscal middleware is designed to protect retailers from country-specific fiscal complexity at the point of sale. It can normalize receipts, fiscal transaction logic, certificates, signatures, fiscal reports, offline handling and communication with local fiscal authorities. That is already a demanding role. Expanding the same layer into full e-invoicing means forcing it to become an ERP extension, an accounts receivable platform, an accounts payable platform, an archive system and a document-exchange hub at the same time.

For a small company with simple flows, that may still look manageable. For an international retailer running SAP or another enterprise ERP across countries, it is difficult to justify. The ERP and accounting system already has the process data, the master data, the invoice logic, the tax determination, the payment connection, the internal controls and the audit trail. Adding another e-invoicing process outside that environment creates more integrations, more reconciliation, more exceptions and more expensive support.

The Hidden Cost of Splitting the Lifecycle

The dangerous part of a bad e-invoicing architecture is not visible on the first project plan. It appears later, when the original invoice is corrected, when a credit note must refer to a previous document, when a platform rejects a submission, when a customer disputes a B2B invoice, when accounts payable receives a self-billed document, when the tax authority expects lifecycle status data, or when an auditor asks why the legally stored invoice in one system does not match the accounting record in another.

At that point, the retailer discovers that e-invoicing is not only about transmission. It is about reconciliation. The original invoice, the correction, the credit note, the payment status, the delivery reference and the archive must all tell the same story. If the POS or fiscalization layer produced one part of the story and the ERP produced the rest, the company needs a control layer to make sure those stories remain synchronized. That control layer costs money, consumes people and creates precisely the kind of operational dependency that the original architecture was supposed to avoid.

This is why a retailer should be careful when a vendor presents e-invoicing as a simple extension of fiscalization. The legal topics may sit next to each other on the tax roadmap, but the process architecture does not sit in the same place. Fiscalization requires tight integration with the sales moment. E-invoicing requires tight integration with the financial document lifecycle.

Returns, Credits and Corrections Expose the Problem

Retailers understand returns better than almost any industry. A return is not merely the reversal of a sale. It can affect inventory, customer service, payments, loyalty, tax, accounting and audit evidence. In e-invoicing, it may trigger a credit note, a corrective invoice, a refund note or another legally defined document, depending on the country and the transaction type.

Spain distinguishes corrective invoices under its invoicing rules. Romania’s RO e-Factura processes corrections and platform responses as part of the regulated flow. Malaysia formally separates credit notes, debit notes and refund notes in the official MyInvois type list. Peppol has dedicated processes for credit notes and self-billing. France is building a system in which lifecycle statuses and e-reporting sit next to e-invoicing. These examples make the same point from different legal traditions. The invoice is no longer just the output of a sale. It is part of a regulated chain of events.

That chain of events is already present in the retailer’s ERP or accounting architecture. It has to be there, because the business cannot close its books, manage receivables, pay suppliers, issue corrections or pass audits without it. Moving only part of that chain to a fiscalization layer does not reduce complexity. It moves complexity into the interfaces between systems.

The Right Architecture Is Separation With Coordination

The right conclusion is not that fiscalization and e-invoicing should never talk to each other. They often must. A fiscal transaction may later become part of a B2B invoice. A return may need to align with fiscal evidence and accounting records. A country may combine fiscal receipt reporting, e-invoicing, e-reporting, SAF-T, certified software, QR codes or transport documentation in one broader tax-control environment.

The correct architecture is therefore separation with coordination. Fiscalization should remain close to the POS and retail transaction layer, where it can handle receipt-level obligations, country-specific fiscal logic, online reporting, certificates, signatures, fiscal devices, offline fallback and immediate store processes. E-invoicing should remain close to ERP, accounting and finance, where it can handle invoice lifecycle events, customer and supplier master data, payment references, credit notes, debit notes, self-billing, archiving, platform statuses and financial reconciliation.

Between the two layers, retailers need controlled interfaces, not duplicated ownership. The fiscal layer can provide clean transaction evidence. The ERP can transform the relevant business event into the correct invoice lifecycle document. The e-invoicing gateway can then exchange, validate, receive, archive and track that document according to the country rules. This is less dramatic than building one universal compliance layer, but it is much safer for global retailers.

Why This Matters for Global Retailers

Most large retailers do not lack systems. They lack clean boundaries. They already run enterprise ERP, accounting, tax engines, POS systems, e-commerce platforms, fiscal middleware, warehouse systems, payment systems and integration platforms. Every additional system boundary becomes a future reconciliation problem unless the ownership model is clear.

That is why e-invoicing architecture should be designed around process reality, not around vendor convenience. If the retailer already has SAP or another mature ERP system owning invoice processes, it should not rebuild those processes inside a fiscalization layer just because one part of the e-invoicing mandate starts with a sales transaction. The cost of duplication will appear in maintenance, exception handling, audit support, data quality and project governance.

For the same reason, fiscalization should not be fragmented across every POS, every country and every e-commerce channel without a strong middleware concept. Retailers need one coherent fiscalization architecture for B2C transaction compliance and one coherent e-invoicing architecture for financial-document compliance. These architectures should exchange data where necessary, but they should not pretend to be the same system.

A Better Product Lesson

For vendors, the product lesson is also important. An e-invoicing product should not be sold as a document converter. It should be presented as an invoice-lifecycle and compliance-exchange engine connected to ERP and accounting. A fiscalization product should not be stretched into every neighboring tax process merely because the same tax authority is involved. It should remain excellent at what it is supposed to do: make retail transactions compliant at the point where they happen.

The future of tax technology will bring more convergence at the regulatory level, but that does not mean every process should converge into the same operational layer. Governments may combine e-invoicing, e-reporting, fiscalization, transport controls, SAF-T reporting and real-time transaction data in a single digital tax strategy. Retailers still need to implement that strategy through systems that match the underlying business process.

In practice, this means that fiscal middleware and e-invoicing middleware can belong to the same compliance landscape without being the same component. They can share knowledge, country intelligence, monitoring, legal updates and governance. They can even be part of the same broader compliance platform. But the transactional ownership should remain clear, because unclear ownership is where global compliance projects become expensive.

The Bottom Line

E-invoicing is much more than B2B sales invoice transmission. It is a regulated lifecycle covering documents, corrections, statuses, receiving, reporting, archiving and evidence. Most of these processes already belong to ERP and accounting systems because that is where the retailer’s financial truth is maintained.

Fiscalization belongs closer to the point of sale because it protects the transaction at the moment it happens. E-invoicing belongs closer to ERP and accounting because it governs the document lifecycle after the commercial event has become a financial and tax record. Mixing the two layers too aggressively may look efficient at the start, but it creates more integrations, more dependencies, more reconciliation and more sources of failure.

The wrong e-invoicing architecture will not only cost retailers money. It will make compliance harder to control. The better architecture is not to force every tax obligation through the same pipe. The better architecture is to understand where each obligation naturally lives, keep the ownership clean, and connect the layers only where the business process truly requires it.

Selected source basis

This article was prepared on the basis of the provided working document on e-invoicing and fiscalization architecture, together with the referenced source landscape around EN 16931 and XRechnung invoice type codes, Peppol Billing and Self-Billing, Italy FatturaPA and SdI, Malaysia MyInvois document types, France e-invoicing and e-reporting lifecycle models, Romania RO e-Factura, Spain corrective invoicing, and Portugal certified invoicing and reporting controls.

EN 16931 / XRechnung invoice type code references, including invoice, credit note, self-billed and payment-related document types. https://easyfirma.net/e-rechnung/xrechnung/codes and https://n4.de/en/blog/e-bill-permitted-formats-in-germany/

Peppol BIS Billing and Self-Billing documentation, including credit notes and self-billed credit notes. https://docs.peppol.eu/poacc/billing/3.0/bis/ and https://docs.peppol.eu/poacc/self-billing/3.0/bis-sb/

Italy FatturaPA and SdI background, including Italy’s structured e-invoicing model and document-type logic. https://www.invoicenavigator.eu/learn/fatturapa and https://developer.b2brouter.net/docs/italian_type_document_codes

Malaysia MyInvois official e-invoice type list, including credit note, debit note, refund note and self-billed document variants. https://sdk.myinvois.hasil.gov.my/codes/e-invoice-types/ and https://sdk.myinvois.hasil.gov.my/types/

France e-invoicing and e-reporting references, including lifecycle statuses and reporting for transactions not covered by domestic B2B e-invoicing. https://entreprendre.service-public.gouv.fr/actualites/A15683?lang=en and https://edicomgroup.com/blog/how-ereporting-works-in-france